General Overview of Commercial Banks

The commercial banks fulfill two primary functions:

- Financial intermediation – bringing together people with money and those seeking to borrow it.

- Operating the check and credit card system via checking accounts.

Financial Mediation

Example:

Mr. Adams has $100,000 available. The bank borrows $100,000 from him, and lends it to the Furnishings Company. The Furnishings Company pays 10% interest to the bank ($10,000 per year) for the use of the money, while the bank pays Mr. Adams 6% interest ($6,000 per year). The bank retains the $4,000 difference. Some of this is used to cover expenses, and the remainder represents the bank’s profit.Generally, lenders to the bank receive lower interest rates as compared with the rates that the bank charges to borrowers who receive loans. The bank profits from the difference.

Operating the Check and Credit Card System Via Bank Accounts

Most of the public receives a monthly salary, and most of this is deposited into a “bank account”, which is also known as a current account. The remaining funds comprised by these salaries are kept in a wallet in the form of bills and coins. When a person wants to buy something, he or she frequently pays by check or credit card, i.e., without using cash.

The Significance of Depositing Cash into a Bank Account

Cash deposited into a bank account is actually being loaned to the bank. This money is placed in the bank vault. At the same time, the bank keeps reports of each bank account by listing the deposits of money in every account. One of Mr. Adams’ account reports is entitled: “Adams – Checking Account”. The statement lists all of his cash deposits and withdrawals relative to that account.

A current balance also appears in the report. In the following illustration you can see Mr. Adams’ bank account statement in the form of a bankbook. The illustrations in the remainder of this chapter portray the bank’s treasury as a vault.

Mr. Adam’s Checking Account Statement

|

Mr. Adams Checking Account ($) |

|||

|

Date |

Deposit |

Withdrawal |

Balance |

|

|

|

|

|

How to read the bank statement?

-

When the balance is positive, we say that Adams has a credit balance. Actually, the bank owes Adams the amount of his balance. In other words, Adams has the right to receive the balance from the bank.

-

When the balance is negative, we say that Adams has a debit balance. Actually, Adams owes the amount of the balance to the bank. A debit balance is indicated by placing the symbol – (minus) or d (abbreviation of the word debit) next to it. For example:

– $500d

– $500.

The following illustration demonstrates a $1,000 deposit by Adams into his checking account on January 1, 2002.

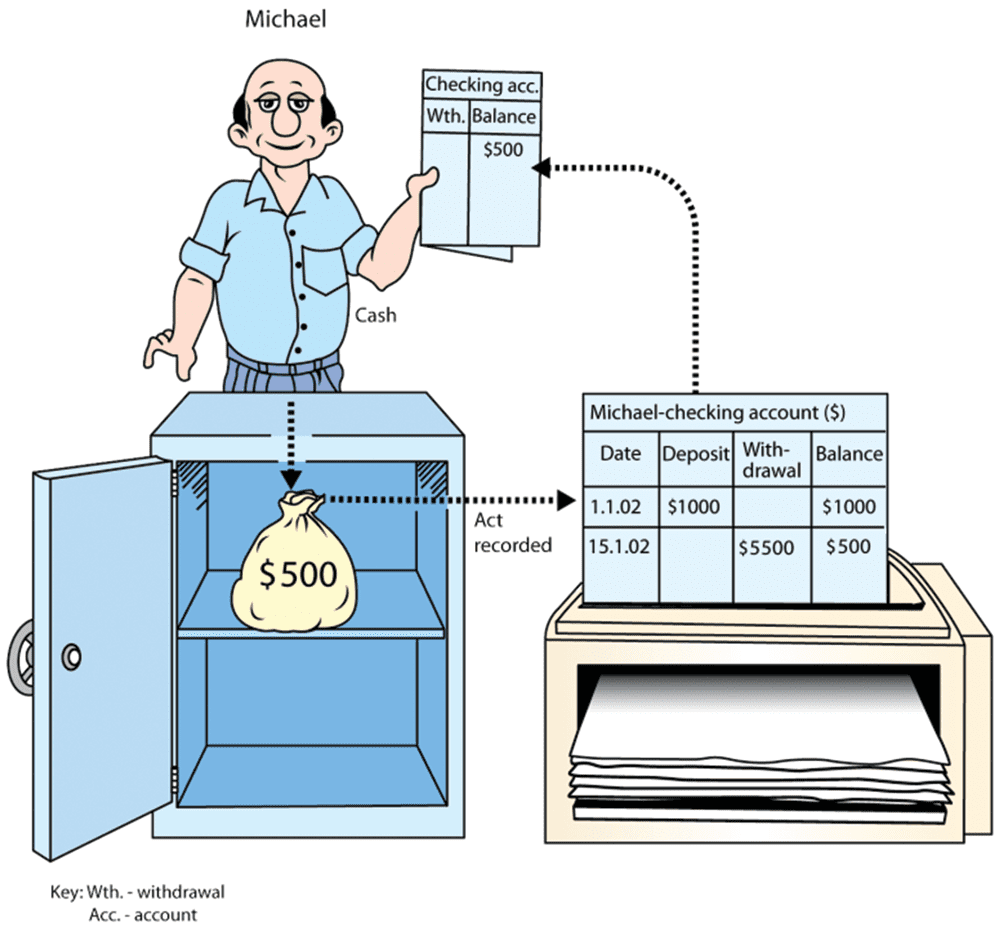

The following illustration portrays a request by Adams for $500 from the bank (or a withdrawal of that amount from an ATM) on January 15, 2002.

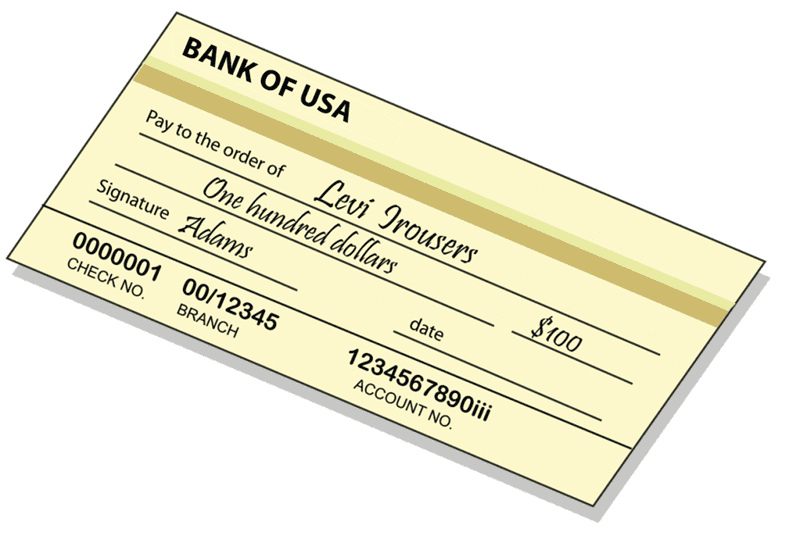

If Adams buys a pair of trousers for $100 and pays for it with a check made out to the order of “Levi Trousers”, he is actually requesting that $100 be transferred from his account into the bank account of “Levi Trousers”. The check is shown in the following illustration.

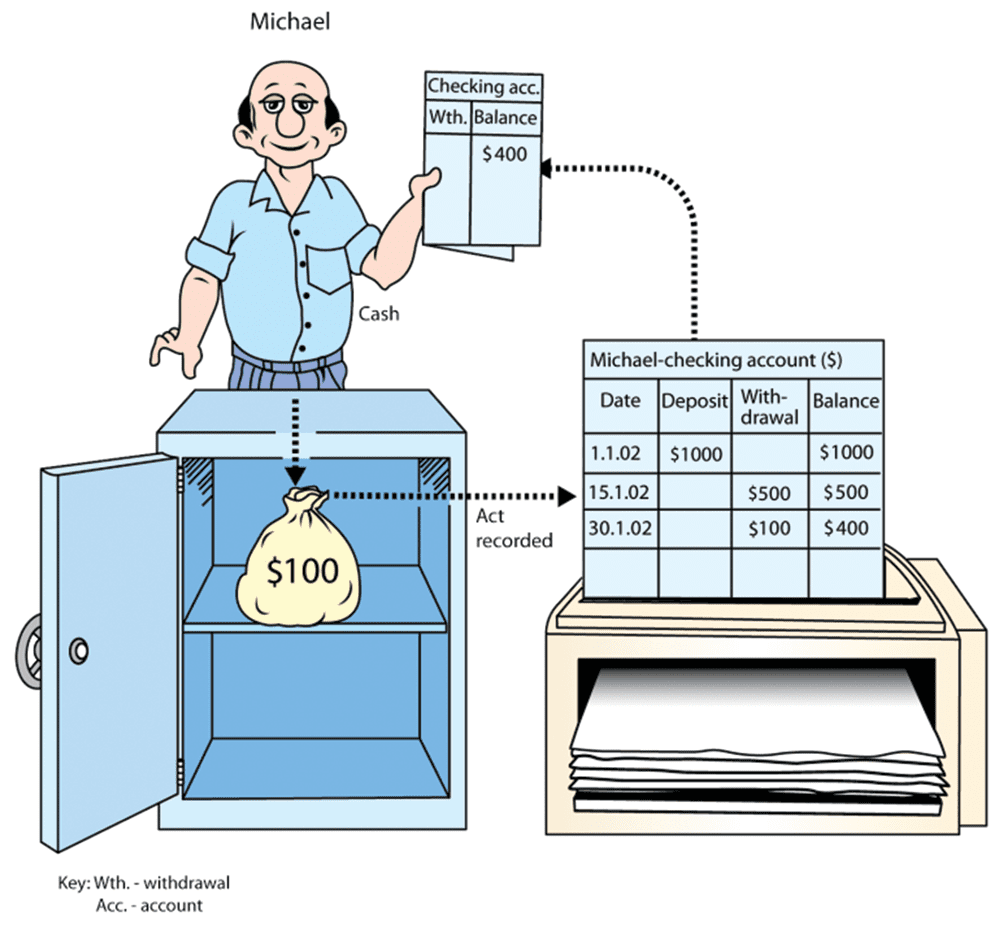

$100 will be transferred from the bank vault to the “Levi Trousers” account and Adams’ checking account balance will decrease by $100 as shown in the following illustration.

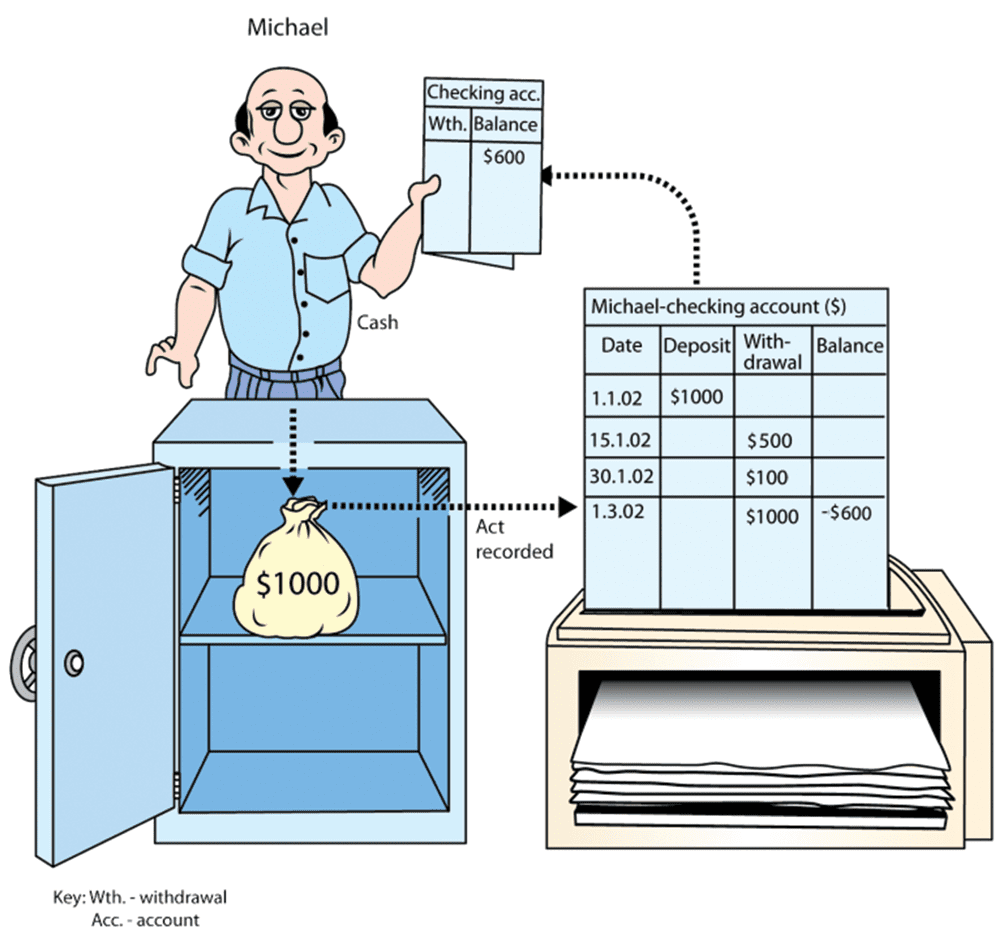

If Adams later (March 1, 2002) buys a table from the Furnishings Company for $1,000 and pays by check, then $1,000 will be removed from the bank vault, i.e., Adams’ bank account would indicate a $600 debit balance. This situation is demonstrated in the following illustration.

Money that is owed to the bank by a customer is called an “overdraft”.