Registration is based on the documents that have been filed in drawers. A ledger file is opened, in which every ledger account represents some drawer, including the virtual drawers (all the ledger accounts are real, including the ledger accounts that represent virtual drawers). Every ledger account is given the name of the drawer that it represents.

The ledger accounts and registration – Examples

- Electricity expenses ledger account Whenever a bill is received from the Electric Corporation, the following particulars of the bill are registered in a single line in the ledger account: Date, period of the bill and total bill amount. During the year, six rows in the ledger account are filled (because the Electric Corporation sends bills once every two months, totaling six per year).

-

Wood purchases ledger account – Every invoice received from each of the enterprise’s wood suppliers will be allocated one row in the ledger account, in which the particulars of the invoice will be registered (date, quantity of wood, sum).

In practice, the registration process is carried out using computer software. The ledger file is a computer file in which the various ledger accounts appear and every transaction is registered in the corresponding ledger account.

The next topic is the Registration System, which provides important background for understanding the subject.

The ledger accounts and registration – Examples

|

Electricity Expenditures Ledger Account |

||

|

Date |

Particulars |

Amount |

|

March 1,2007 |

Electricity expenditures Between January and February 2007 |

$1,000 |

|

May 1, 2007 |

Electricity expenditures Between March and April 2007 |

$1,500 |

|

July 1, 2007 |

Electricity expenditures Between May and June 2007 |

$1,200 |

|

Sept. 1, 2007 |

Electricity expenditures Between July and August 2007 |

$1,800 |

|

Nov. 1, 2007 |

Electricity expenditures Between September and October 2007 |

$1,500 |

|

Jan. 1, 2008 |

Electricity expenditures Between November and December 2007 |

$1,000 |

|

Wood Purchases Ledger Account |

||

|

Date |

Particulars of the Purchase |

Amount |

|

Jan. 1, 2007 |

Purchase of wood from Africa Wood – 50 kg of planed wood |

$1,000 |

|

June 1, 2007 |

Purchase of wood from Great Wood – 100 kg of complete wood |

$2,000 |

|

Oct. 1, 2007 |

Purchase of wood from Africa Wood – 150 kg of complete wood |

$3,000 |

|

Dec. 1, 2007 |

Purchase of wood from Bench Wood – 100 kg of natural wood |

$2,000 |

Registration System in Double Entry Bookkeeping – Explanations and Examples

Introduction

The technique of registration is actually a technical system operated by a bookkeeper. Familiarity and thorough understanding of it are not essential for someone who is not planning to work as a bookkeeper him/herself. Only a short general explanation of the method will therefore be given.

The registration system is called double entry.

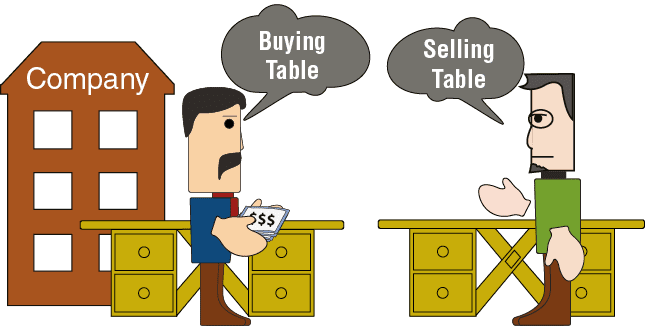

This system is based on the fact that two sides are involved in every business operation: One side gives, and the other side receives. Each side is represented by a bookkeeping ledger account. A limited liability company is required to use double entry bookkeeping.

Examples

- The company bought wood from Africa Wood The company received wood. The Africa Wood company supplied wood. This transaction is registered in two ledger accounts: Wood Purchases and Africa Wood. Registration in the Wood Purchases ledger account reflects the wood received by the company. Registration in the Africa Wood ledger account reflects the wood supplied by Africa Wood.

- The company sold tables to Central Furniture.Central Furniture received tables. The company supplied tables. The two ledger accounts involved in this registration are Table Sales and Central Furniture. Registration in the Table Sales ledger account reflects the tables sold. Registration in the Central Furniture ledger account reflects receipt of the tables.

-

The company received a bill from Electric Corporation – A brief explanation: Registration in the Electricity Expenditures ledger account reflects the electricity received by the company. Registration in the Electric Corporation ledger account reflects the electricity supplied by the Electric Corporation.

-

The company paid the Electric Corporation – The two ledger accounts involved in the transaction are the company’s Current Account and the Electric Corporation. The registration in the Current Account Ledger Account represents the expenditure of cash. The registration in the Electric Corporation Ledger Account represents the receipt of cash.

|

Ledger Accounts |

||

|

Table Sales |

|

Central Furniture Ltd. |

|

Ledger Accounts |

||

|

Electric Corporation |

|

Electricity Expenditures |

|

Ledger Accounts |

||

|

The company’s current account |

|

Electric Corporation |

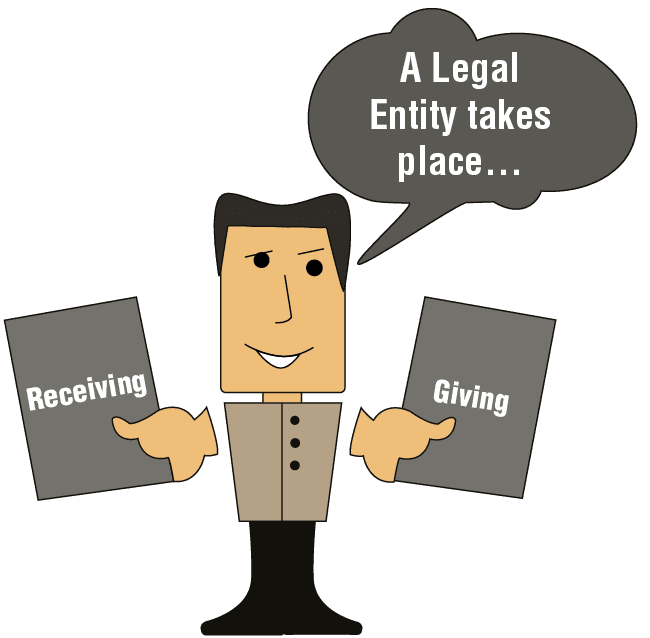

Transaction Process in a Ledger Account by a Legal Entity – An Explanation

In order to better understand “giving” transactions and “receiving” transactions, it is important to realize that in double entry bookkeeping, interaction takes place in every business transaction. Registration in one ledger account always represents “receiving”, while registration in another ledger account represents “giving”. This will become clearer when the method of registration is explained.

In some of the ledger accounts in which the “receiving” of any sum of money is registered, “giving” of the amount received is also registered at a later time. On the other hand, in some of the ledger accounts in which the giving of any sum of money is registered, receiving of the same sum of money is also registered at a later time.

For the purposes of this explanation, ledger accounts will be treated as people who both give and receive. In professional terms, each of the imaginary people is called a “legal entity”. In every transaction, the bookkeeper’s job is to identify the account ledger in which the receiving will be registered, and the ledger account in which the payments will be registered.