Marginal Cost Definition

When we produce quantities of a certain item, the cost of the last item produced is called the marginal cost.

Understanding Diminishing Marginal Returns

Diminishing marginal returns is a popular term in Economics and it relates to the decrease in the production output. First, let us explain what we mean by output. Output represents the quantity of products produced during a specific time period. For example, if we build two chairs per hour, our output is two chairs per hour. If we make six chairs in two hours, then in terms of output per hour, our output is three (6 / 2 = 3 chairs) chairs per hour. The term diminishing marginal returns describes a phenomenon with two results, both of which are different aspects of the same phenomenon:

-

Output declines over time.

-

It takes more time to make each additional product.

If one chair is produced in one hour at the beginning of the day, and output is halved during the day, then it takes two hours to produce a chair at the end of the day. Economists believe that diminishing marginal returns exists in most industrial and agricultural sectors, meaning that it takes longer to produce each additional item. Since hourly wages are fixed, then the cost of manufacturing each additional item also rises.

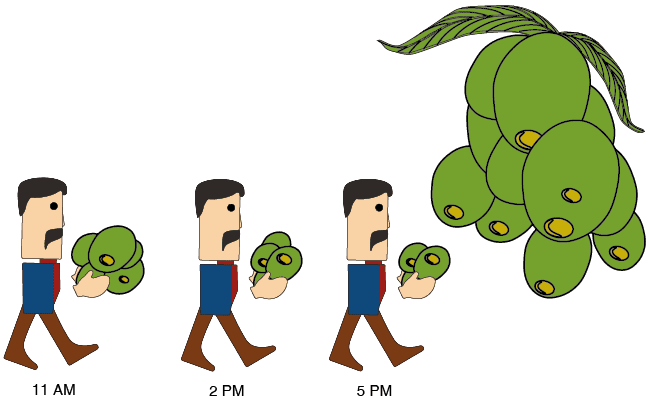

An Example of Diminishing Marginal Returns

When the harvest season arrives, Mr. Johnson hires a family of four to help him to pick olives. The family charges two dollars per minute of labour. The workers get progressively more tired during the day (due to Diminishing Marginal Returns), so it takes more time to pick each additional ton of olives. The workers also need work breaks, and these breaks become longer as the day progresses. The following table displays the cost of olive picking for Mr. Johnson, and the amount of olives actually harvested.

Table 2.1

|

Total amount of olives picked |

Total work time |

Total cost |

Average cost per ton |

Marginal cost per ton |

|

Column 1 |

Column 2 |

Column 3 |

Column 4 |

Column 5 |

|

1 ton |

60 minutes |

$120 |

$120 |

$120 |

|

2 tons |

130 minutes |

$260 |

$130 |

$140 |

|

3 tons |

210 minutes |

$420 |

$140 |

$160 |

|

4 tons |

300 minutes |

$600 |

$150 |

$180 |

|

5 tons |

400 minutes |

$800 |

$160 |

$200 |

|

6 tons |

510 minutes |

$1020 |

$170 |

$220 |

How to read Table 2.1:

Start with Row 3. Picking three tons of olives (Column 1) takes 210 minutes (Column 2), and costs $420 dollars (Column 3). The average cost per ton, calculated by dividing the Column 3 by Column 1, is therefore $420 divided by three tons = $140 (Column 4).

Column 5 – Marginal cost :

The marginal cost is the cost of picking the last ton of the total quantity picked. For example, the marginal cost of the third ton is $160. We arrive at this figure by subtracting Row 2 from Row 3 in Column 3 (the numbers in the circle). When the total quantity of olives rises from two to three tons, (i.e. when we pick the third ton), costs increase from $260 to $420. The cost of the additional ton (also called the marginal ton) is $160.