Understanding how rating agencies rate corporate bonds.

It is difficult for an individual investor to evaluate the ability of a company to repay its bond and to meet the payments that it undertook when the bond was issued. For this purpose, there are agencies that specialize in the evaluation of companies and their ability to repay their debts to investors. These companies rate the bonds in order to provide investors with a professional assessment of an issuer’s ability to repay their debts. The lower the risk (i.e., the lower the probability that the company will go bankrupt and fail to repay its debt), then the higher the company’s rating will be. It therefore follows that the higher a bond’s rating is, then the lower the interest that the bond will pay since the probability that the company will fail to meet its obligations is lower, and investors will require less compensation for their investment in the company. Conversely, it is also true that the lower a bond’s rating (meaning that the debt is riskier), then the higher will be the compensation that investors will demand for their investment in the bond, resulting in a higher interest rate.

Note that a rating is given for a specific bond or a series of bonds. The rating is not for a company. It is certainly possible that a company issuing a number of bonds will receive different ratings for the various bonds.

The rating granted by the rating agencies concerns a specific debt. Among the considerations that rating agencies take into account are the purpose for which the money (i.e., the debt) has been raised and the quality of the guarantees. It is certainly possible for one debt to relate to more speculative purposes, while another debt concerns a more substantial project, which would consequently be less risky.

Similarly, it is possible that different debts have different guarantees (i.e., a certain series may be backed by a guarantee, while a different series may not). In addition, the rating of a bond may be revised depending upon changes in the company. A company may encounter economic difficulties, its management may be replaced, etc. A change in the rating of a bond is a significant event, and may have consequences for the yield that the bond is expected to generate.

A number of bond rating companies operate in the US, but only three rating agencies: Moody’s, Standard & Poor’s (S&P), and Fitch have been granted the status of authorized rating agency by the American Securities and Exchange Commission.

Every rating company has a rating ladder with a number of rungs, which are listed as follows. S&P and Fitch’s ladders have 10 levels, while those of Moody’s have nine levels. The rating ladder is presented in descending orderfrom the highest rating to the lowest. At some of the levels, there is an internal rating based upon a uniform format (+/- or 1,2,3).

|

|

Fitch |

S&P |

Moody’s |

|

1. The lowest level of risk |

AAA |

AAA |

Aaa |

|

2. Far below average level of risk |

AA+ AA AA- |

AA+ AA AA- |

Aa1 Aa2 Aa3 |

|

3. Lower than average level of risk |

A+ A A- |

A+ A A- |

A1 A2 A3 |

|

4. Average level of risk |

BBB+ BBB BBB- |

BBB+ BBB BBB- |

Baa1 Baa2 Baa3 |

|

5. Higher than average level of risk |

BB+ BB BB- |

BB+ BB BB- |

Ba1 Ba2 Ba3 |

|

6. Far above average level of risk |

B+ B B- |

B+ B B- |

B1 B2 B3 |

|

7. Extremely high level of risk |

CCC+ CCC CCC- |

CCC+ CCC CCC- |

Caa1 Caa2 Caa3 |

|

8. A real chance of insolvency |

CC |

CC |

Ca |

|

9. The issuer is on the verge of insolvency |

C |

C |

C |

|

10. The issuer is insolvent (the internal rating reflects the probability that the issuer will emerge from insolvency) |

DDD DD D |

D |

|

Division of the Ratings into Two Groups

Individual investors are not the only ones who have difficulties evaluating the quality of each company’s debt. Investment institutions also make use of evaluations by rating companies for the purpose of assessing the attractiveness of corporate investments. Ratings can be divided into two groups:

-

An investment grade group.

-

A speculative grade group.

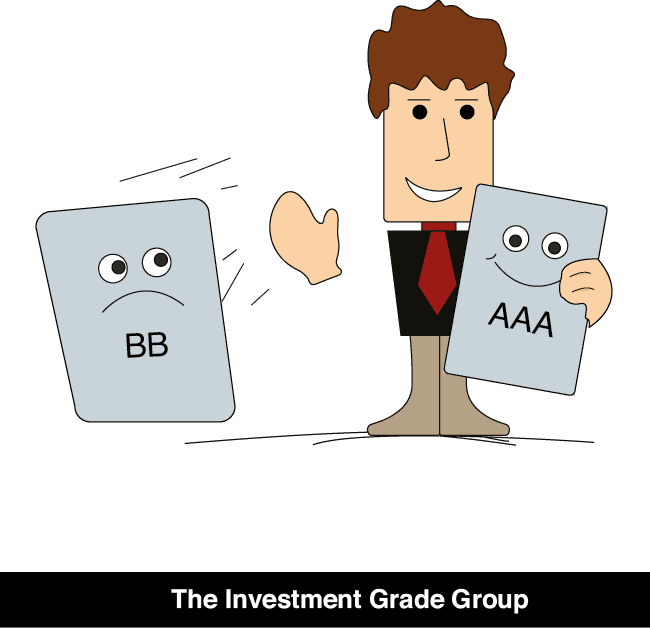

The Investment Grade Group

The four highest ratings – AAA, AA, A, and BBB – constitute the preferred group. They are referred to as investment grade, which means that the series receiving these ratings have a sufficiently low risk for investment purposes. Large investment institutions in the U.S are prohibited from buying bonds with ratings lower than BBB.

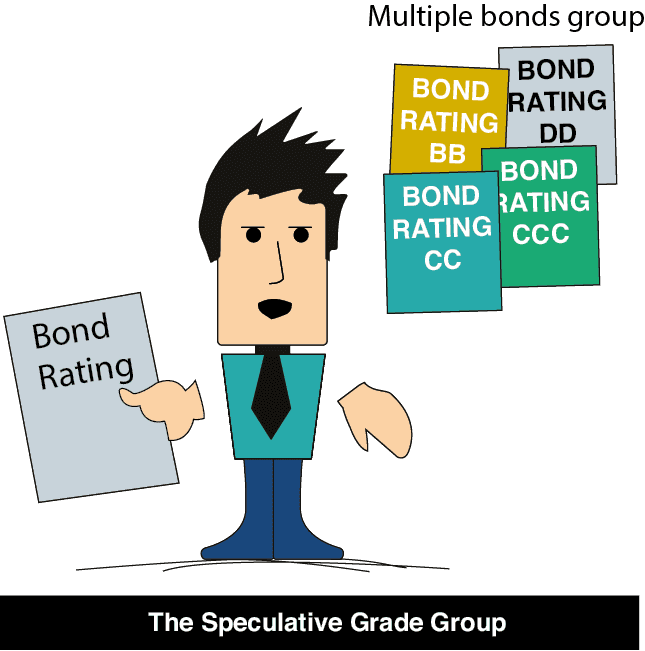

The Speculative Grade Group

All ratings of BB or lower are included in this group.

Since the ratings of bonds affects the yields that they generate (i.e., the compensation that investors demand for the use of their money), the bond ratings make it possible to compare the bond yields according to similar standards and to invest in bonds with higher yields. This helps to prevent distortions due to investments in bonds with high yields, but also high risk.

Voluntary Rating

Credit rating companies assess most new bond series in the market on their own initiative, and they update their ratings as and when needed. This rating is performed without any payment by the issuers, and is based upon publicly disclosed information.

Paid Ratings

If a bond issuer wishes to reveal some information to the rating company that has not been publicly disclosed, they must pay for the rating. It is clear that issuers choose this alternative only when they believe that providing this additional information would be advantageous.

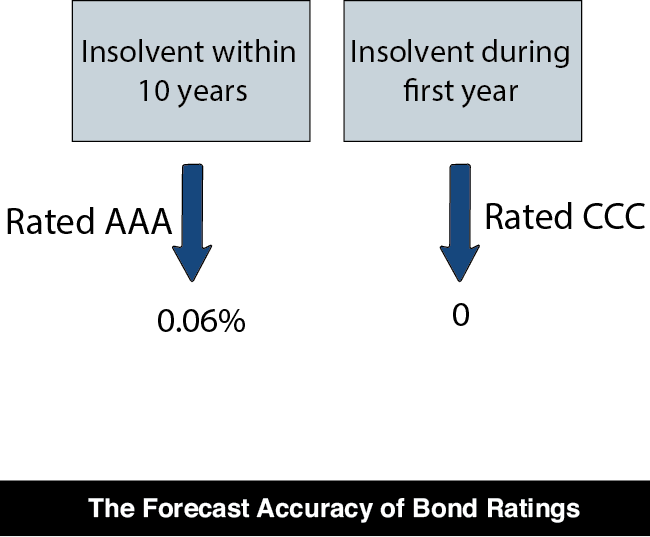

The Forecast Accuracy of Bond Ratings

The financial community usually attributes great importance and complete objectivity to the bond ratings provided by the three authorized rating agencies. Empirical studies show that the ratings applied to bonds are usually an accurate reflection of their strength in the long term. For example, in the 27 years between 1971 and 1997:

-

Among the corporate bonds that were rated AAA upon their issue by S&P, no bond series went insolvent during the first year after issue, and only 0.06% of these bonds were afflicted by insolvency (i.e. an inability to repay the obligations stemming from the bonds) within 10 years of their issue.

-

Among all of the the bonds that were rated CCC by S&P, 2% were afflicted by insolvency during the first year after their issue, and 47% were experienced insolvency within 10 years of their issue.

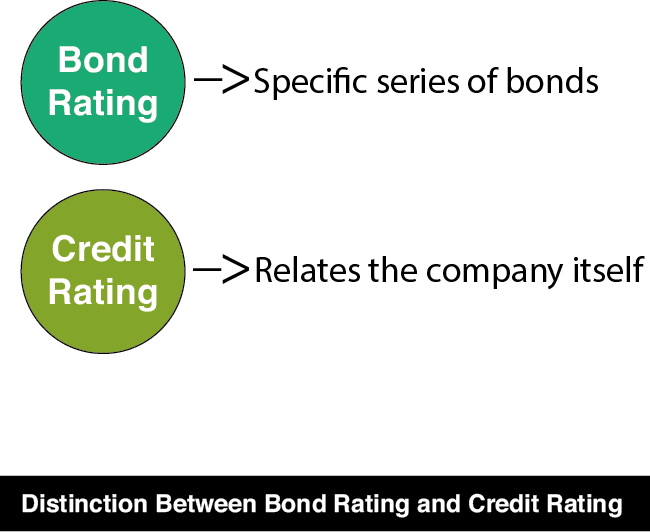

Distinction Between Bond Rating and Credit Rating

It is important to distinguish between bond rating and credit rating. A bond rating relates to a specific series of bonds. A credit rating, on the other hand, appraises the company itself, and is designed to assist creditors (i.e., banks, bondholders, etc.) in evaluating the company’s ability to meet the full range of its financial obligations.